Compare domestic oil prices

Since Summer 2014, oil costs have fallen about 65per cent in United States dollar terms (about $70) as growth has progressively slowed across an easy array of nations. This outcome features puzzled numerous observers including us at the Fund, who'd believed that oil cost decreases will be a net plus when it comes to globe economy (IMF 2015), demonstrably hurting exporters but delivering more-than-offsetting gains to importers.

Since Summer 2014, oil costs have fallen about 65per cent in United States dollar terms (about $70) as growth has progressively slowed across an easy array of nations. This outcome features puzzled numerous observers including us at the Fund, who'd believed that oil cost decreases will be a net plus when it comes to globe economy (IMF 2015), demonstrably hurting exporters but delivering more-than-offsetting gains to importers.

The key presumption behind that belief could be the assumed difference between saving behavior of oil importers versus oil exporters.

- If oil importers save 10 cents regarding dollar while exporters save 20 dollars, moving a single dollar of earnings from exporters to importers boost global usage.

For instance, whenever an oil cost fall transfers $1 of earnings, worldwide usage rises by 90 cents (the excess use of importers) less 80 cents (the usage reduction by exporters). A net increase of 10 cents in international consumption may be the outcome.

- The conventional belief that an oil cost fall is perfect for the whole world economic climate after that uses through the declare that generally speaking, consumers in oil-importing regions including European countries have actually a greater marginal propensity to eat that people in exporters such as for example Saudi Arabia, that could run down its wide range or borrow to cushion short-term declines in export profits.

Stock areas aren't convinced: could be the low interest rate environment at fault?

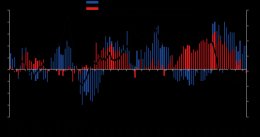

Demonstrably, globe equity markets have-not purchased this principle (Blanchard and Acalin 2016). Over the past half a year or even more, equity markets have tended to fall whenever oil costs fall – not that which we would anticipate if lower oil costs assist the globe economy on balance. certainly, since August 2015 the simple correlation between equity and oil costs hasn't just been good (Figure 1), it offers doubled in comparison to an earlier duration starting in August 2014 (though to not ever an unprecedented level).

certainly, since August 2015 the simple correlation between equity and oil costs hasn't just been good (Figure 1), it offers doubled in comparison to an earlier duration starting in August 2014 (though to not ever an unprecedented level).

Figure 1 stock exchange and oil costs

(60 times moving house windows of day-to-day return correlation)1

Note: 1 Correlation between WTI oil cost and MSCI USA return. Horizontal red lines suggest the common correlation for the corresponding periods.

Resource: Datastream.

Past symptoms of sharp alterations in oil prices have actually had a tendency to have visible countercyclical impacts – for example, reduced globe development after big increases (Hamilton 2009). Is it time various? A number of elements affect the relation between oil rates and development, but we're going to believe a positive change from previous episodes is many higher level economies have actually nominal rates of interest at or near zero.

Supply versus need

One apparent issue in forecasting the effects of oil cost moves usually a fall-in the planet price might result often from an increase in international offer or a decrease in worldwide need. However in the next instance, we might expect to see identical pattern as with recent quarters – dropping costs accompanied by slowing global development, with lower oil rates padding, but likely perhaps not reversing, the growth slowdown.

One apparent issue in forecasting the effects of oil cost moves usually a fall-in the planet price might result often from an increase in international offer or a decrease in worldwide need. However in the next instance, we might expect to see identical pattern as with recent quarters – dropping costs accompanied by slowing global development, with lower oil rates padding, but likely perhaps not reversing, the growth slowdown.

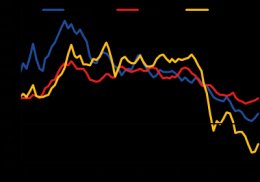

Figure 2 Commidity cost indices

(2005=100)

Source: IMF, Major Commodity Cost system.

Slowing demand isn't any doubt an element of the story, but the proof suggests that increased offer are at minimum as important. One telling indicator is the different behavior of costs of oil as well as other products.

- If oil prices reflect a generalised fall-in worldwide need, after that with similarly good deal elasticities of supply, we'd anticipate various other commodities to show a price course much like oil’s.

But that's not more or less the truth.

Metals began their particular drop in 2011 with the beginning of Asia’s rebalancing and growth slowdown – China consumes up of 50percent of global supply of some metals – and decline happens to be almost regular (Figure 2). In razor-sharp contrast, the fall-in oil started only in the last half of 2014, and it has already been much steeper as compared to decline in other commodities since that time.

More typically, oil supply is strong due to capture high result from OPEC users including, now, exports from Iran, along with from some non-OPEC countries. Besides, the united states way to obtain shale oil in the beginning proved amazingly resilient in the face of reduced costs. Figure 3 reveals exactly how OPEC output has recently proceeded to develop as rates have fallen, unlike in certain earlier rounds.

More typically, oil supply is strong due to capture high result from OPEC users including, now, exports from Iran, along with from some non-OPEC countries. Besides, the united states way to obtain shale oil in the beginning proved amazingly resilient in the face of reduced costs. Figure 3 reveals exactly how OPEC output has recently proceeded to develop as rates have fallen, unlike in certain earlier rounds.

FIgure 3 World oil production development

(Change in million drums every single day produced, unless mentioned usually)

Note: APSP (average petroleum area cost): easy avg. of British Brent, Dubai Fateh and western Tx Intermediate.

Resource: IMF, Primary Commodity cost Sytem; IEA and IMF staff computations

Additionally, even in the US – a net oil importer in which need has-been fairly powerful – low priced oil seems to not have given a substantial fillip into the development rate. Econometric also scientific studies (Arezki and Blanchard 2015) declare that only area of the current drop in oil is because of slowing demand – somewhere within a half (Baumeister and Hamilton 2015) and a third (World Bank 2015) – using balance taken into account by increasing supply.

Generally there remains a puzzle.

In which on the planet can the results of lower oil rates be seen?

To deal with this question, we compare the 2015 and 2016 domestic need growth in oil importers and oil exporters that we projected in April 2015 – following the very first substantial decline in oil costs – to the 2015 outturn plus the 2016 projection through the most recent, April 2016 World financial Outlook. The April 2015 forecast for oil rates was somewhat above actual costs for that 12 months, but had been greater for 2016 and beyond. Consequently, absent other bumps, you might have expected the most recent WEO forecasts to exhibit stronger performance in oil importers, particularly for 2016, and weaker performance in oil exporters.

- The lion’s share for the downward modification for international need originates from oil exporters – despite their reasonably small share of global GDP (about 12%).

- But domestic demand in oil importers has also been no better than we had forecast, despite a fall in oil rates that was a lot bigger than expected.

See also:

- ?u yollarla para kazanmak Halal Finance Genel Bak??

- Все про боль в спине на сайте https://vashaspina.ru/, заходи читай!

Share this article

Related Posts

Latest Posts